Consumer spending has declined sharply during the pandemic, even for households that have not experienced a fall in income. For policy-makers seeking to stimulate the economy, it is important to understand what are the main drivers of diminished consumption.

The Covid-19 pandemic has triggered an unprecedented spike in job loss and fears about a potentially deep and persistent recession, largely due to depressed consumer spending. Given the important role of consumption in the UK economy, it will be crucial to understand the determinants of diminished spending in order to design policy to support households during the pandemic and guide the country out of recession.

Who has decreased spending and by how much?

Transaction-level spending data for the UK show that consumer spending has fallen substantially during the pandemic, not only for people who suffered job loss or a fall in income, but also for those who have not (Hacioglu et al, 2020). This evidence also shows that higher earners (those in the top 25% of incomes) cut their expenditure more than any other income group, and by more than the fall in their incomes. Similar patterns have been found in the United States and Spain (Chetty et al, 2020; Carvalho et al, 2020).

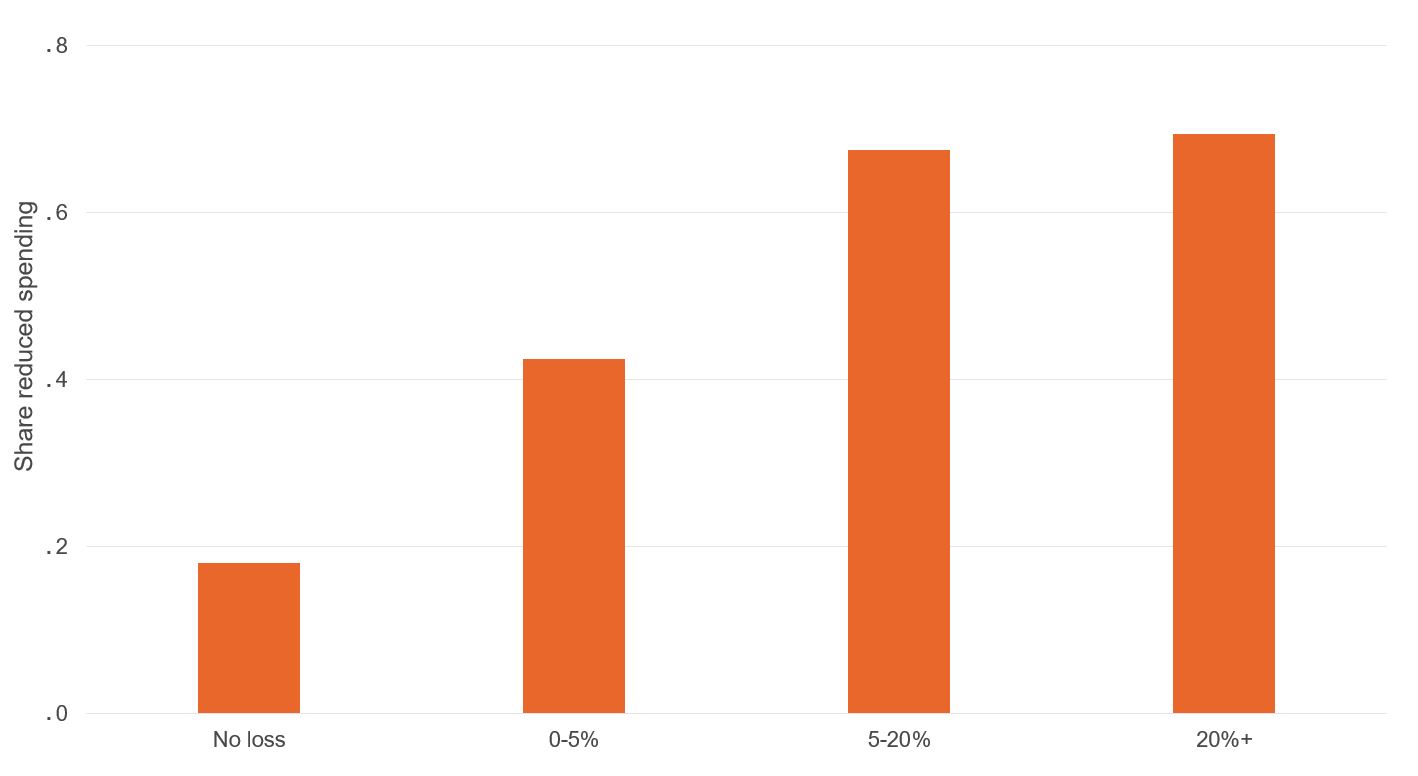

Surveys of UK households, such as Understanding Society, point to similar results. Figure 1 shows that among those with no decline in earnings, 20% report a reduction in spending. The probability of reduced spending is higher for those who also experience an earnings decline, but the observation that spending falls across the board suggests factors other than a loss of income must be at play (Benzeval et al, 2020).

Figure 1: Fraction Reducing Spending by Household Income Decline

Notes: Reproduced from Benzeval et al (2020). The x-axis groups individuals based on the size of household income loss.

What are the reasons for spending changes?

For those who experience a decline in earnings, there is a direct effect. Reduced income will lead to reduced consumption, particularly for those without other means of finance such as savings, borrowing or help from friends and family. This decline in consumption will depend on how long the reduction in income is expected to last: the shorter the duration, the easier it is for a household to maintain its desired consumption plans.

In addition to this direct effect, there are three further effects on households that have experienced an income fall as well those that have not:

- Supply restrictions: Restrictions on access to goods and services, which may include restrictions imposed on businesses by lockdown and social distancing, as well as supply chain disruptions.

- Demand changes: Shifts in preferences that may be due to health concerns that make particular services – such as eating out – less attractive. More generally, reduced demand due to a desire or need to self-isolate.

- Increased uncertainty: Concerns over the future may lead individuals to defer spending. These concerns may be over future employment prospects or, more generally, future income.

Any fall in spending will have implications for saving rates: for those without a change in income, reduced consumption leads to extra saving. For those whose income has declined alongside consumption, it is unclear whether savings will go up or down.

During all recessions in the UK over the past 40 years, the fall in consumer spending has led to a rise in saving (Crossley et al, 2013). This increased saving and decline in aggregate demand can exacerbate rises in unemployment.

Related question: Why is uncertainty so damaging for the economy?

Which reasons for decline are most prevalent?

Our framework identifies three key channels for changes in consumption in addition to the direct effect of the income decline. Disentangling the different channels underlying the decline in spending is important for assessing which policies might be best suited for stimulating the economy.

One way to disentangle supply versus demand effects is to compare spending responses across similar countries that have imposed different restrictions. Denmark and Sweden provide a good point of comparison (Sheridan et al, 2020).

Denmark had a government-mandated lockdown, whereas Sweden did not. Spending dropped by around 29% in Denmark in the early weeks of the crisis, while in Sweden, the decline was only 4 percentage points smaller. The authors of this study conclude that the primary reason why spending fell is because of changes in demand caused by fear of the virus itself.

Moreover, changes in demand depend on the degree to which different individuals would be affected by the virus. With Denmark and Sweden, there are striking differences between the two countries in how the size of the spending response varies by age. The young have a larger fall in spending in Denmark where supply restrictions are binding, whereas the old have a larger fall in spending in Sweden, perhaps due to health concerns reducing demand.

The conclusion from this work is that avoiding lockdown (or other supply restrictions) is not sufficient to prevent the potential economic catastrophe induced by the pandemic (see Munday and Surico, 2020). Furthermore, there are notable spending dynamics caused by the severity of lockdown: a more severe initial lockdown may have better long-run consequences by reducing longer-run dampening of demand.

The differential dynamic effects can be seen by comparing the performance of the United States and France during the spring and summer of 2020. France had tighter restrictions in March and April, leading to a sharper reduction in spending during these early months. But by the summer of 2020, the French economy was rebounding by more than the US economy (Bounie et al, 2020).

There is a further question of whether changes in demand are induced by current restrictions or by uncertainty about future job prospects. A full analysis requires data on spending responses by occupation because different sectors face different risks.

While these data are not yet available, research points to the effects of uncertainty on precautionary savings. Studies have found that individuals cut back spending after a friend loses their job and that higher risk of job loss causes a substantial increase in savings (Sheridan, 2019; Juelsrud and Wold, 2019).

How can policy help and how does it depend on the reasons for reduced consumption?

To answer this question, we focus on options to increase consumer spending. Since different countries have taken different approaches, we compare experiences to understand which policies might have the biggest effects. We focus on policies that operate through stimulating demand rather than those aimed at boosting supply.

The United States has brought in direct stimulus payments, which went to all citizens and permanent residents, with the amount increasing for those with children. The US government also increased both the size and duration of unemployment benefits, which should have different effects on spending from the direct stimulus payments because unemployment payments go to a targeted subset of the population.

The UK reduced value added tax (VAT) on the hospitality sector from 20% to 5% between July 2020 and March 2021, and also introduced the ‘Eat Out to Help Out’ scheme for the month of August. This scheme was an additional subsidy to eating in cafes and restaurants between Mondays and Wednesdays.

In addition, the UK provided direct payments through the Coronavirus Job Retention Scheme (CJRS), which worked to maintain the pay of those who would otherwise be working zero hours. A similar scheme supported the self-employed. Additional schemes have offered mortgage holidays and rent protection.

We can categorise policy measures for stimulating demand into three groups:

- Pay support: Policies that boost income to households.

- Price support: Policies that change prices for particular goods.

- Reducing uncertainty: Policies that provide insurance, tamping down future uncertainty.

Pay support

Policies that provide additional income to households, as in the United States, lead to increased spending, although there is substantial variation across households.

There is evidence that stimulus payments during the Covid-19 crisis have been particularly effective in boosting consumption for households with low liquid assets, lower incomes and greater declines in income (Baker et al, 2020). By contrast, stimulus payments during the crisis have had less effect on spending for households with high bank account balances or little reduction in income.

This evidence suggests that one of the best ways to boost consumption is to target support at those who have lost income due to the pandemic or who had limited resources going into the pandemic. A natural way to do this is through increasing welfare payments, such as Universal Credit in the UK, or by extending the duration of job furlough schemes.

Price support

Policies that change prices operate in a different way. Rather than boosting income-related spending, price changes induce households to switch to the good that is being subsidised. This switch may be from spending on other goods in the same time period, or bringing forward spending that had been planned for a point in the future.

Being specific, we can think of the Eat Out to Help Out scheme as a policy intended to induce substitution of spending away from supermarkets and takeaways, as well as away from saving. But there are likely to be substantial unintended substitutions too: for example, away from eating on other days of the week towards those days that are subsidised; or away from other sorts of purchases.

A further issue with this particular scheme is that it represents a subsidy towards less safe forms of spending. Recent research shows that the sudden increase in physical interactions due to this scheme may have contributed to the recent upsurge in Covid-19 infections (Fetzer, 2020).

Reducing uncertainty

It is also important to implement policies that reduce job and income uncertainty for households that may otherwise feel a need to cut back on spending for precautionary reasons. Two examples of such policies include the CJRS in the UK and the extension to unemployment benefits in the United States.

In addition to providing direct cash assistance, these schemes also reduce uncertainty over future job prospects, which may be negatively affected by the pandemic. The difficulty is that such schemes have inevitably been short-term and the uncertainty over future job prospects is increasingly being seen as a long-term, persistent problem.

Dealing with this sort of uncertainty requires long-term income protection policies, but this may sit awkwardly alongside a need for sectoral reallocation. Countries like Denmark, which already have comprehensive social insurance schemes, are likely to see the benefit of these schemes – the uncertainty channel is going to be much more muted in those countries.

An alternative policy response has been to allow access to savings that have been locked away, such as in pensions. For example, the CARES Act in the United States allows households early access to their 401(k) retirement accounts. This follows an example set by countries such as Denmark, which released pension savings in 2009 in order to stimulate consumer spending (Kreiner et al, 2019). For individuals who have lost income, this can provide resources to help maintain consumption and living standards during the crisis.

In addition, early access to pension savings can boost spending among households that have not suffered a fall in income. There is evidence that households suffer from temptations that make it difficult to accumulate wealth (Kovacs et al, 2020). As a result, pensions may serve as a savings ‘commitment device’ due to their illiquidity. Policies that provide early access to pension savings may temporarily break the commitment device and boost consumer spending (Kovacs and Moran, 2020). This policy represents a trade-off: lower saving for retirement in the name of a short-run boost to aggregate demand.

Finally, there is an important distinction between demand stimulus policies that are targeted towards a narrow sector of the economy versus more broadly. For example, the Eat Out to Help Out scheme in the UK is particularly targeted towards the hospitality sector. In contrast, the CARES Act in the United States seeks to boost consumer spending more broadly.

The former is more appropriate when the impact of lost demand is short-lived, in which case increased spending will help businesses to survive. The latter is needed when the impact is longer-lived because the boost in spending can lead to new jobs even in areas not initially affected by the pandemic.

Where can I find out more?

- Social distancing laws cause only small losses of economic activity during the COVID-19 pandemic in Scandinavia: Discussion of the evidence on the impact of supply restrictions.

- COVID-19 survey: the economic effects: Summary of individual-level consequences of Covid-19 by the Institute for Social and Economic Research

- Consumption in the time of Covid-19: Evidence from UK transaction data: CEPR study by Paolo Surico, Sinem Hacioglu and Diego Kaenzig.