A big rise in government borrowing has been an essential policy response to the health and economic effects of Covid-19. History indicates the importance of supporting the economic recovery rather than worrying about what is a temporary shock to the public finances.

The UK public finances are undergoing a crisis of a magnitude that we have not previously seen outside wartime. Between April and June 2020, a quarter of the working population was laid off or furloughed in an attempt to prevent the spread of Covid-19, and although some of those jobs have returned, we are still far from a full recovery. Those layoffs led to a loss in output and a spike in the government’s deficit as the Treasury borrowed to compensate those who lost their jobs or were asked to stay home to safeguard the health of the vulnerable.

There is a danger that the Chancellor will feel pressure to reverse the spike in public borrowing quickly by raising taxes too soon and by cutting back on public sector pay awards. That would be a mistake.

Government finances are not like household finances and there are very good reasons why repayment for a temporary expenditure on an event like Covid-19 relief should be spread out over a long period of time (Farmer and Zabcyck, 2018). There are also good reasons to encourage a short period of above average inflation. Raising taxes and curbing public sector pay increases are not the right ways to pay equitably for the public health crisis.

Figure 1: Weekly hours in the UK

Source: ONS

Figure 1 illustrates the magnitude of the blow that the economy was dealt. This chart shows that weekly hours worked fell by almost 20% from February to June 2020, and although the labour market has begun to recover, we are a long way from a return to full employment. The uptick we see in these data is unlikely to continue as the second national lockdown will surely delay the recovery.

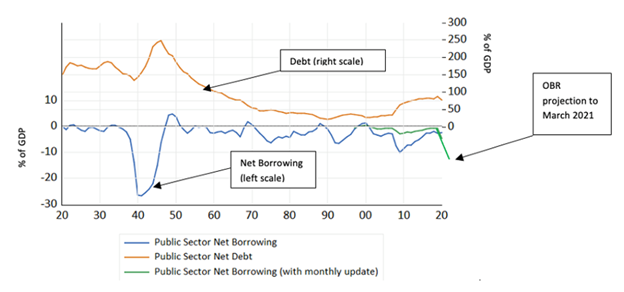

The magnitude of the hit to the public finances is illustrated in Figure 2, which plots national debt as a percentage of GDP (the orange line measured on the right scale) and net public sector borrowing (the blue line measured on the left scale). The annual data are supplemented with monthly data projected forward to March 2021 in the green line also measured on the left axis. What do these data mean and how bad is it?

Figure 2: UK debt and deficits since 1920

Source: ONS and author's calculations

The short answer is: don’t panic, we have had much higher debt-to-GDP ratios in the past and we will likely have much higher ratios again in the future. The Office for Budget Responsibility (OBR) estimates that cumulative annual borrowing might be close to £350 billion by the end of the fiscal year; that is about 18% of GDP and although large, it is not unprecedented. As we see from Figure 2, public sector borrowing was above 20% for five years in a row during the Second World War.

Are we in a wartime situation? In a sense, yes. Government borrowing rises during wartime to spread the cost of paying for a war over future as well as current generations. Covid-19 is similar and it has been expensive to the public purse for a reason. We collectively chose to compensate those who were laid off or furloughed to keep the rest of us safe. In wartime, there are fewer consumption goods to go around because the nation pulls together to produce armaments. In the Covid-19 crisis, there are fewer consumptions goods to go around because we are asking 20% of our fellow citizens to stay home.

The people who have suffered economically are predominantly young and poor. They are the unemployed single parents who have been furloughed and are living from one support cheque to the next. They are not the journalists, office workers, and academics who are able to continue to work from home and are mildly inconvenienced from the inability to dine out at our favourite restaurants. But it would be a mistake to think that higher taxes and reduced public sector pay raises are a necessary consequence of our collective decision to help the vulnerable. We can, and should, spread out the repayment period for this decision over decades.

To understand how to pay for the Covid-19 crisis, consider how we paid for the Second World War. Figure 2 shows that the government has been a net borrower for almost all of the post-war period. This is reflected in the fact that the blue line, which measures government borrowing, is below zero for almost every year. But government debt (the orange line on the chart) continued to fall in every year from the end of the war in 1946 right up to the onset of the global financial crisis in 2008.

Debt, measured as a percentage of GDP, continued to fall even as the government borrowed more money every year. This is not unusual. It is a systemic feature of the public finances of many sovereign nations and it happened because the interest rate at which the UK government repaid its debt was lower than the growth rate in its ability to repay.

If your income grows at 5% per year forever but the interest on your credit card is 3%, you can you continue to borrow more every year and your debt, measured relative to your income, will still continue to shrink. That is what happened to the UK Treasury and it is a feature that is unlikely to go away soon.

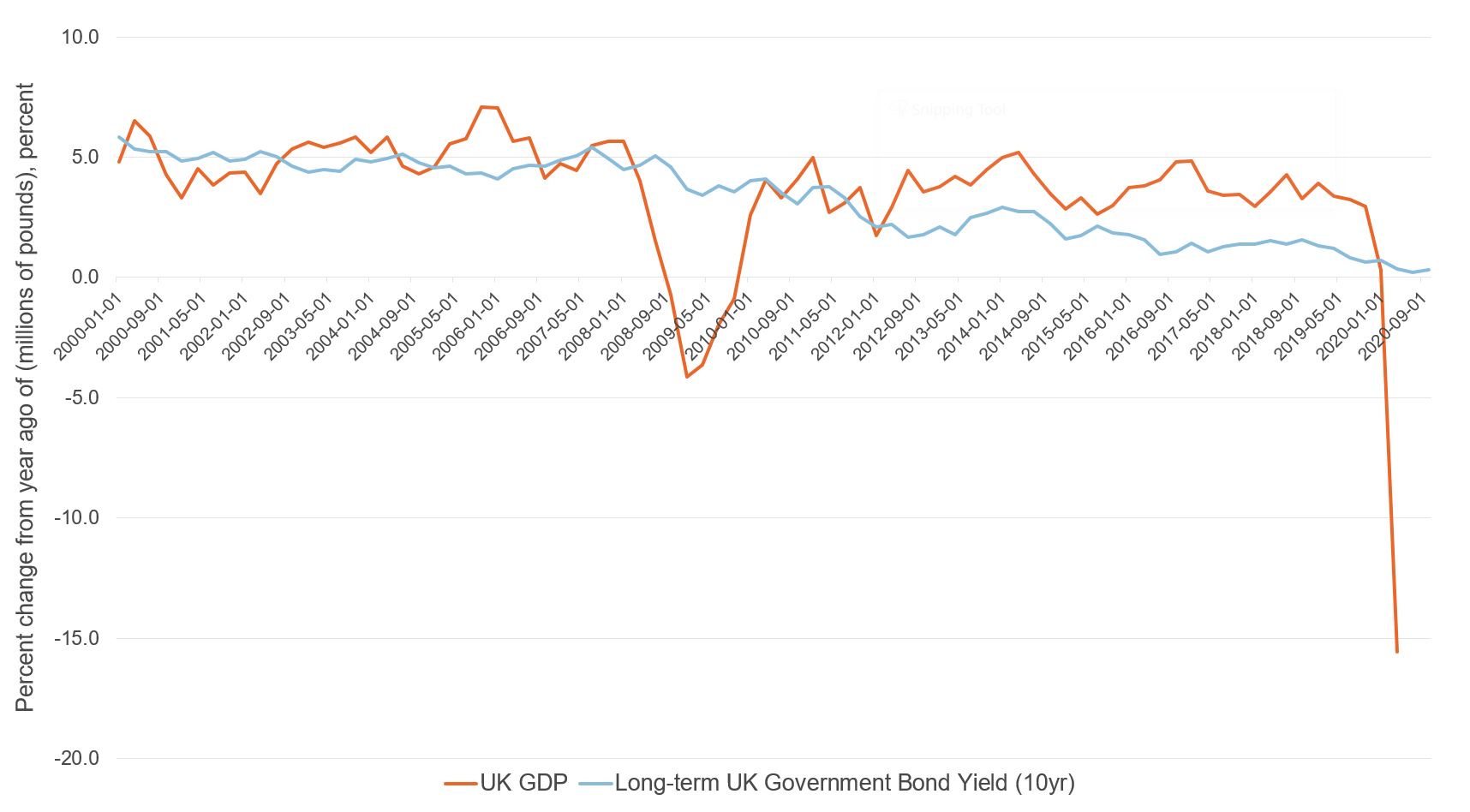

Figure 3: Nominal GDP growth and the yield on 10-year government bonds since 2000

Source: ONS & OECD

Figure 3 plots the rate of growth of nominal GDP and the yield on ten-year government bonds. GDP growth is the red line and the bond yield is the green line. Both series are measured from the first quarter of 2000 to the third quarter of 2020. The chart shows that, with the exception of the global financial crisis of 2008/09, the ten-year bond yield was consistently lower than the GDP growth rate.

The most recent Covid-19 crisis is a second exception but history tells us that, once we emerge from the recession, GDP growth will rebound and the Treasury will again be able to borrow without imposing additional tax increases and without cutting back on public sector pay awards.

Although Covid-19 is bad, it is not unprecedented. The Spanish flu of 1918 killed a quarter of a million people in Britain alone, with an estimated mortality rate of between 10% and 20%. More people died in 1918 of influenza than in the four years of the bubonic plague from 1347 to 1351 and it was particularly lethal among those in the 20-30 year age group.

Covid-19, by comparison, is most deadly to the elderly. But even in this vulnerable group, the survival rate is estimated by the US Centers for Disease Control and Prevention (CDC) to be greater than 99.5% (CDC, 2020). Covid-19 is bad. But we have weathered much worse.

There is good news. There are now at least three vaccines on the horizon – two with 95% effectiveness and one with 70% effectiveness – and the announcement of these advances suggests that the lockdowns will be over soon.

The economy will recover on its own. The government should not try quickly to pay off the accumulated debt by raising taxes or cutting back on spending as that will likely delay the recovery. It should not be afraid to allow an increase in public sector wages. Wage increases are a necessary precursor to a temporary increase in price inflation that will help to distribute a reduced supply of consumption goods to the population.

Are there any circumstances in which the government should contemplate tax increases or expenditure reductions? If it is planning to increase government transfers permanently, then yes, taxes may need to be raised to pay for them. But that is unlikely to be a wise choice. People do not want permanent handouts: they want jobs.

If the government is planning a permanent increase in infrastructure investment to rebuild the North; that should be paid for by borrowing, not by tax increases. Infrastructure investments, if wisely chosen, will pay for themselves.

In the meantime, it is important to let the economy recover and not listen to ‘deficit hawks’ who fret needlessly over what is a temporary shock to the public finances.

Where can I find out more?

- The Household Fallacy: Roger Farmer and Pawel Zabczyk explain why we should be sceptical of the idea that government must 'tighten its belt' as a necessary policy response to higher indebtedness.

- Reducing high public debt ratios: lessons from UK experience: Nicholas Crafts studies how the UK public debt has been reduced in the past.

- Fiscal policy after the referendum: Jagjit Chadha writing in the National Institute Economic Review.

- Managing the UK national debt 1694–2018: Martin Ellison and Andrew Scott look at UK debt management using a monthly dataset on the quantity and market price of every individual bond issued by the government since 1694.

Who are experts on this question?

- Roger Farmer

- Jagjit Chadha

- Nicholas Crafts

- Andrew Scott

- Tatiana Kirsanova