It is now common for companies to report their performance on a variety of environmental, social and governance (ESG) indicators. But their use in socially responsible investing is currently held back by a lack of transparent and consistent ratings of corporate practices.

Corporate performance on environmental, social and governance (ESG) issues has been gaining attention in global financial markets. Where in the past, companies’ main focus might have been to maximise profits for shareholders (Friedman, 1970), now they are increasingly recognising that being environmentally, socially and ethically responsible also has the potential to be good business.

To this end, many firms are amending their articles of incorporation to ensure that they are balancing profit with purpose. For example, certification provided by the B-Corps – a global movement driven by community leaders advocating the use of business as a force for good – is a trending phenomenon for companies that seek to demonstrate their commitment to being ethical and environmental. Certified B-corporations are legally required to meet the highest standards of verified ESG conduct. Their number has grown from 85 in 2007 to well over 3,500 by 2021.

This increase suggests that companies are becoming more ESG conscious, with many undertaking initiatives and adopting new policies that are environmentally friendly, socially responsible, publicly transparent and sound in legal accountability – while maintaining the goal of maximising profitability. Actions include carbon reduction initiatives, recycling and waste management, a transition to using renewable energy, and greater representation of women and ethnic minorities on corporate boards.

As such, corporate reporting on ESG matters – through annual reports, websites and press releases – is now becoming a mainstream practice for companies to showcase their improved environmental and social performance. This also serves to attract not just a sustainability-minded customer base, but also financing from socially responsible investors (Khan, 2019; Cort and Esty, 2020). The number of public corporations reporting on ESG matters has grown from fewer than 20 in the early 1990s to well into the thousands today (Kotsantonis et al, 2016).

Corporate reporting on ESG metrics presents the central inputs for rating agencies to conduct measurement and assign ratings. Examples of these metrics include a firm’s carbon emissions, land use, data security, supply chain labour standards and tax transparency (see Figure 2 for more).

High ESG ratings are perceived to reflect good sustainability conduct; conversely, low scores represent poor performance. The ratings are then used by investors in the screening and evaluation of socially responsible investments (Widyawati, 2020).

Some argue that the intricate and inherently subjective nature of sustainability makes it difficult to gauge, therefore rendering ESG metrics as a valid but inadequate proxy (Edmans, 2021). Their view is that sustainability is not something that can be measured but rather assessed, which requires supplementing the quantitative ESG ratings with qualitative company-specific information. This could include, for example, the industry or sub-industry in which the company operates or the extent of ESG operations compared with industry peers (Edmans, 2020).

Over-focusing on quantitative ESG metrics may also distort investors’ understanding of the real extent of sustainability efforts, which would, in turn, lead corporations to over-invest in those with short-term payoffs. For investors to create long-term value, they need to go beyond the quantitative ESG metrics and look into the contextual aspects of a given firm (Edmans, 2021).

Do ESG metrics affect firm performance?

A report by Calvert Research and Management, an investment management company, lists a number of ways in which good ESG conduct can lead to enhanced financial performance for firms (Serafeim et al, 2015).

First, corporate environmental initiatives lead to less waste, improved energy efficiency and fewer environmental fines and damages – all of which translates into cost savings and higher profit margins.

Second, the efficient handling of natural resources can be viewed by investors as a reliable indicator of a firm’s management of other resources. This may boost investors’ confidence and enhance corporate value by means of higher stock returns and/or lower cost of capital.

Third, good ESG conduct can generate higher revenues by drawing in a new customer base and providing for previously unserved parts of the population with the introduction of environmental products or green process innovation (for example, the use of recycled and/or recyclable packaging).

Fourth, sustainability practices can have a positive effect on corporate reputation and brand values, which, in turn, enhances long-term value creation by attracting a more talented and engaged workforce, as well as more satisfied and loyal customers.

In short, a sustainable firm will stand to benefit from good ESG conduct with enhanced competitive advantage (from product or process innovation, and customer satisfaction), higher revenues from efficiencies and cost savings, and lower cost of capital and/or higher market valuation by virtue of less exposure to operational, legal and reputational risks (Serafeim et al, 2015; Kotsantonis et al, 2016; Lanza et al, 2020).

One study reports that above average ESG performers show higher expected growth, lower cost of capital and higher valuation multiples in the stock market (Serafeim et al, 2015), although the study did not look closely at what are considered ‘material’ ESG issues.

Another study focuses on a small subset of ESG data as the material and hence ‘value-relevant’ ESG issues for each industry (Kotsantonis et al, 2016). This approach is the underlying premise of the efforts of the Sustainability Accounting Standards Board (SASB), which aims to identify material ESG issues for nearly 80 different industries and to propose reporting standards for each (Kotsantonis et al, 2016).

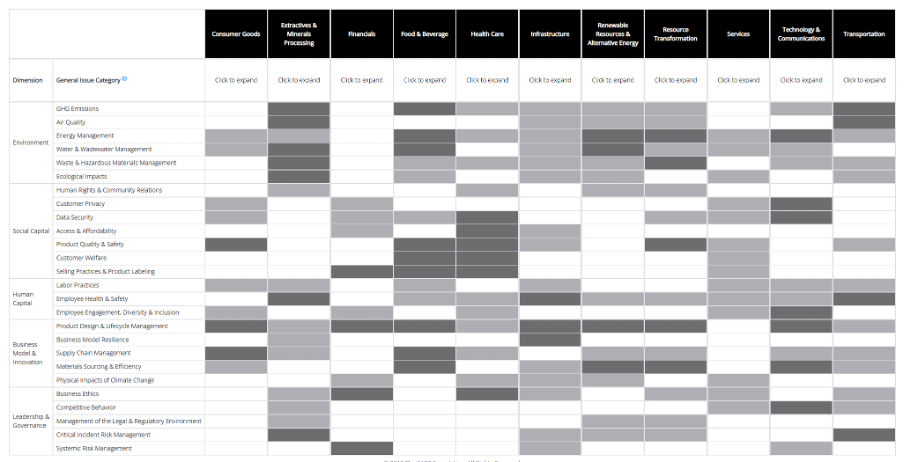

For example, the management of environmental issues (including waste management and greenhouse gas emissions) is considered material for fossil fuel and transport industries but immaterial for financial and healthcare industries. Other ESG concerns (for example, fair marketing and advertising) are considered important (material) for financial and healthcare industries. SASB’s materiality map shows a detailed breakdown of material ESG investments that affect financial conditions and operating performance within an industry.

Figure 1: SASB materiality map

Source: SASB

One study takes on the SASB’s distinction of industry-based material ESG issues and reports that firms making major investments in material ESG issues experience significant payoffs, with increases in profit margins and higher risk-adjusted stock returns than their counterparts (Khan et al, 2016). The same study also reports that firms making significant investments in SASB-based immaterial ESG issues were associated with average or, in some cases, even inferior financial performance.

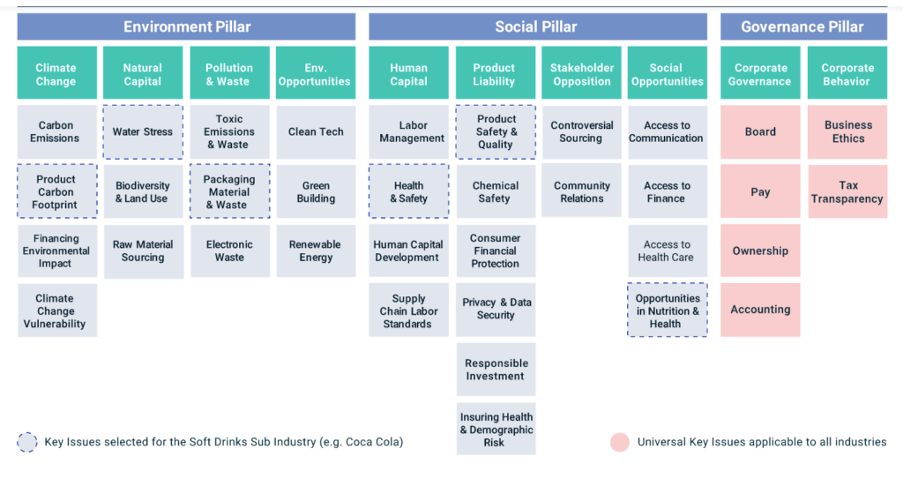

This underlines the importance of distinguishing material industry-related ESG investments from immaterial, though perhaps socially popular, ones. The former bears positive effects on long-term firm value while the latter has neutral to negative effects. Figure 2 shows an example of industry-specific material ESG data for the soft drinks industry.

Figure 2: The components of MSCI's ESG score

Source: MSCI (2021)

How are ESG metrics driving the growth of the market for socially responsible investing?

Increasing recognition of the importance of environmental, social and governance issues has given rise to a new investment management approach that integrates (material) ESG metrics alongside traditional financial metrics – such as return on investment and net present value. The integration of ESG metrics into the mainstream investment management is recognised as responsible investing or socially responsible investing (Gary, 2019; Widyawati, 2020).

The market for socially responsible investing has grown considerably over the last 15 years. By the end of 2019, over 4,000 signatories that manage more than $80 trillion in assets had signed the United Nation Principles for Responsible Investment (UNPRI), compared with just 100 signatories in 2006 (UNPRI, 2021). Figure 3 shows the growth of UNPRI signatories and the respective amounts of assets under their management.

Figure 3: PRI growth, 2006-2021

Panel A: Assets under management

Panel B: Number of signatories

Source: UNPRI (2021)

The notable growth of UNPRI signatories highlights the increasing momentum of responsible investors in global efforts to achieve the Sustainable Development Goals. ESG metrics are considered as an essential prerequisite in establishing and developing the market for socially responsible investing (Widyawati, 2020).

ESG ratings render socially responsible investing understandable and scalable to the broader financial community. They help to ensure not only the growth but also the legitimacy of socially responsible investing as an emerging market (Widyawati, 2020). In particular, they extend legitimacy since they are widely seen as a valid proxy for corporate sustainability performance, which, in turn, can accelerate the growth of emerging markets for socially responsible investing (Widyawati, 2020).

For example, the establishment of the UK’s Ethical Investment Research and Information Service (EIRIS) in 1983 is credited as one of the main factors enabling the growth of the UK market for socially responsible investing (Solomon et al, 2004). Similarly, the French market for socially responsible investing grew substantially after Arese (an ESG rating agency later known as Vigeo Eiris) was established in 1997 (Arjaliès, 2014).

The accelerated growth of the market for socially responsible investing as a result of introducing ESG metrics is amplified when accompanied by compatible regulations. For example, mandatory disclosure of greenhouse emissions, compulsory compliance with a certain governance code and/or adoption by key market players (for example, institutional investors and/or largest listed corporations) are all factors that can amplify the effect of ESG metrics on accelerating growth of the market for socially responsible investing. Such growth can also be dampened by lack of transparent and consistent ESG metrics (Vasudeva, 2013; Kreander et al, 2015; Juravle and Lewis, 2008).

ESG metrics: many providers but little transparency and consistency

There are many recognised agencies providing ESG metrics or ratings. The KLD ratings of KLD Research & Analytics, Inc – a former US agency, now owned by MSCI ESG Research LLC – are arguably the oldest and most popular source of ESG ratings. Recently, more US and Europe-based agencies are starting to provide their own ratings, including: ASSET4 (now acquired by Thomson Reuters), Bloomberg, Vigeo Eiris, RobecoSAM (now acquired by S&P Global Ratings), Sustainalytics and ISS-Oekom.

Unlike the KLD ratings, which provided binary-based ESG metrics (in other words, a yes or no type of rating), the newer agencies employ more elaborate and in-depth proprietary methodologies in ranking ESG performers. More specific criteria for each dimension are established, binary codes are expanded, weights are assigned and reassessed for each criteria and dimension, and then, an aggregate score is provided (Widyawati, 2020).

Despite the sophisticated underlying measurement methodologies, these ESG metrics remain flawed (Kotsantonis et al, 2016; Widyawati, 2020; Cort and Esty, 2020). The lack of transparent, standardised and consistent measurement methodologies continues to have problematic implications for the market for socially responsible investing. Even changes in the market of ESG information providers exacerbate transparency concerns with the launch of each new agency (Delmas et al, 2013). This is the case as each new agency that enters the profession employes a unique rating index and assigns ranks that are different from those assigned by other agencies.

The lack of clear and quality standards in the measurement of ESG ratings poses questions about the accuracy of these metrics and the extent to which they capture a company’s true environmental, social and governance performance (Kotsantonis et al, 2016; Widyawati, 2020; Cort and Esty, 2020).

As such, investors are continuously reminded to exercise caution when using ESG metrics (Widyawati, 2020). They can be obscure, quantitative and highly subjective assessments (Edmans, 2020). Investors are also advised to supplement them with qualitative company-specific information if long-term value is to be created (Edmans, 2021).

While there appears to be a growing convergence on industry-related material ESG issues, alignment on common metric definitions and measurement methodologies is yet to have developed (Kotsantonis et al, 2016; Khan et al, 2016; Cort and Esty 2020). The criteria used by the various ESG rating agencies for industry-specific materiality remain unclear and arbitrary. This highlights the need for a standardised framework to codify the procedures of conducting material risk assessments (Cort and Esty, 2020).

There is a need to coordinate the existing efforts and build on the work of the global reporting initiative, the SASB and many others to establish high quality standards for providing ESG ratings. Standardised guidance on data specifications and measurement methods is an essential prerequisite for reliable and consistent ESG ratings.

Where can I find out more?

- The social responsibility of business, Alex Edmans (2015)

- The dangers of sustainability metrics, Alex Edmans (2021)

- Social Responsibility Perspectives: The Shareholder and Stakeholder Approach, Alanis Business Academy (2014)

- Accounting: The Friedman conundrum, Stephen Bouvier (2021)

- Who’s afraid of stakeholder capitalism? Vivian Hunt (2021)

- Rising temperatures, melting ratings, Patrycja Klusak et al (2021)

Who are experts on this question?

- Lane Matthews

- Matthew Agarwala

- Patrycja Klusak

- Alex Edmans