The effects of coronavirus and lockdown on the economy have been very large: UK GDP fell by a record 20.4% in the second quarter (April to June 2020). New data indicate how this economic shock is playing out across the different parts of the country.

There are two sources of official data that can help us to consider the immediate effects of the Covid-19 crisis at the local level: the claimant count; and government data on the local take-up of different income support schemes.

Both these sources of data show wide and varying local economic effects. These data sources come with important caveats, which means that there is still considerable uncertainty over the immediate local economic effects. Once again, the Covid-19 crisis is highlighting the problem of obtaining accurate and timely economic data for local areas.

Claimant count

The claimant count consists of administrative data that measure the number of people claiming benefits because they are unemployed and seeking work. It is a composite of the number of people claiming Jobseeker’s Allowance (JSA) and those on Universal Credit (UC) who are required to seek work to qualify for their benefits.

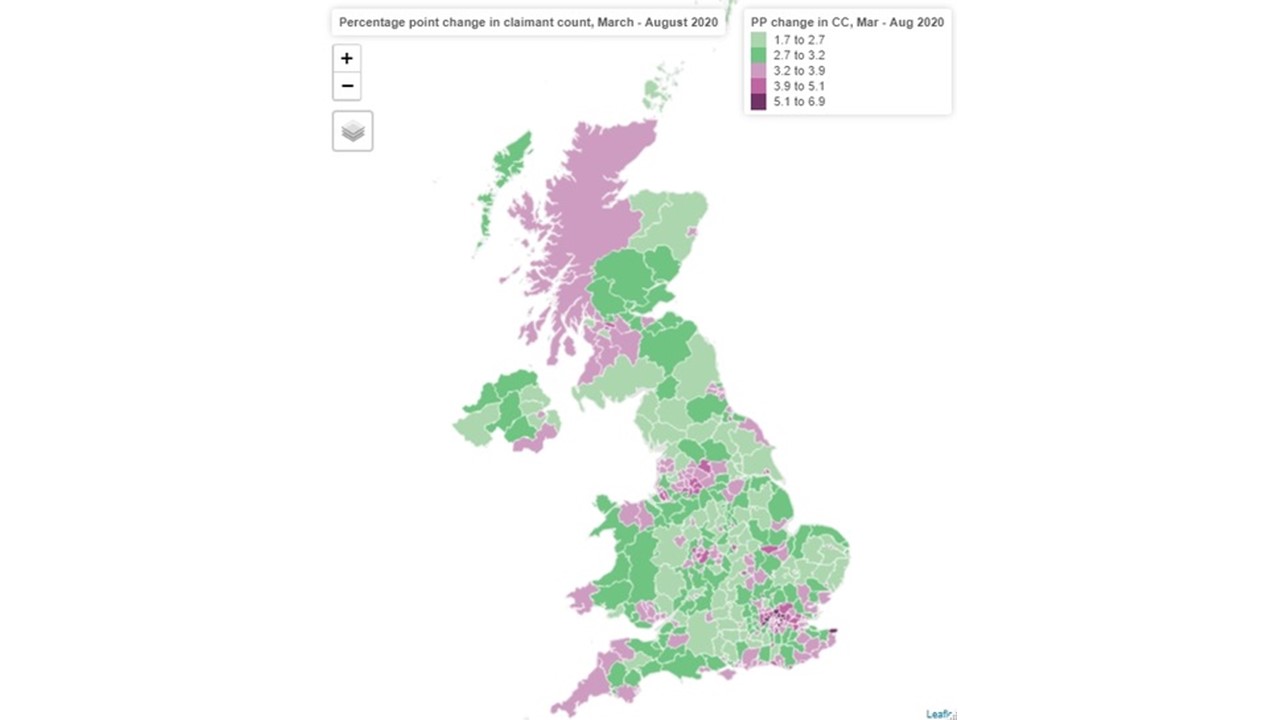

Figure 1 shows the local authorities experiencing the largest and smallest percentage point changes in claimant count between March (the last data pre-lockdown) and August (the latest data available, released on 15 September).

Figure 1: Percentage point changes in claimant count from March to August 2020 by local authority

Source: Mapped by Thomas Sells, Centre for Cities using data from the Office for National Statistics: Claimant Count data March and August 2020 and Population Estimates 2019 (latest data available).

Do the claimant count data give a good indication of the local economic effects?

The introduction of UC had already caused some issues for claimant count data. The UC count includes any recipient required to look for work (a broader definition of ‘unemployed’ than under JSA). As a result, the claimant count has increased since UC was included.

More important for using claimant count as a measure of the local economic impact of Covid-19 are changes to UC that the government made in response to the crisis. These measures increased the number of employed people eligible for UC because their earnings fall below income thresholds.

In addition, in some cases, the salary of employees supported by the Coronavirus Job Retention Scheme (CJRS) may be reduced making them eligible for UC although still employed. This means that some of the increase in claimant count could be due to people being furloughed on reduced income. The Office for National Statistics (ONS) currently has no way of knowing how much of the current caseload is due to employed or unemployed claimants.

Area variation in the claimant count may also be affected by variation in the up-take of the CJRS. Workers who would otherwise have been laid off and claim benefits, but whose jobs have been protected by CJRS will not show up in the claimant count.

Related question: How does the government's furlough scheme work?

Coronavirus Job Retention Scheme

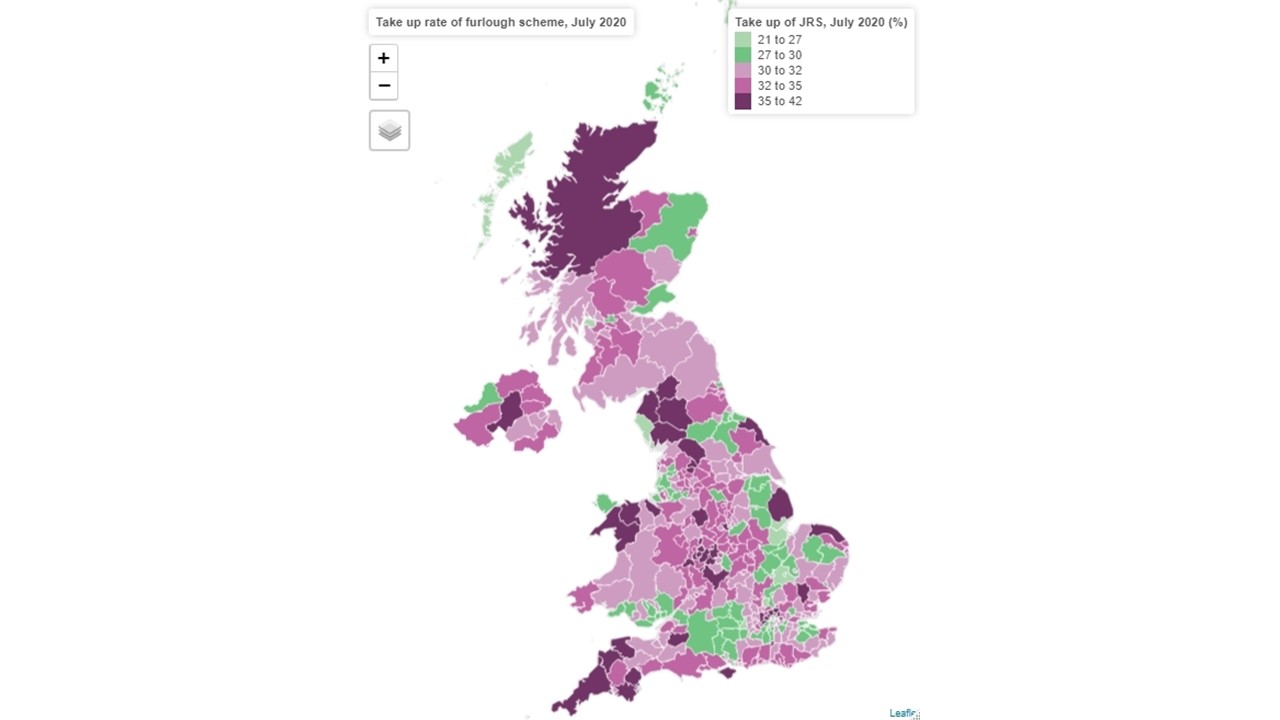

On 21 August, HM Revenue and Customs released the cumulative data on the local take-up of the CJRS up to the end of July. As with the claimant count, the data reveal a great deal of variation in take-up across the country. At the national level, approximately 32% of the workforce has been furloughed for at least one three-week period since the introduction of the scheme in March. Figure 2 gives the variation by local authority.

Figure 2: Take-up rate for the Coronavirus Job Retention Scheme from March until the end of July 2020

Source: Mapped by Thomas Sells, Centre for Cities using data from HM Revenue and Customs: Job Retention Scheme statistics by local authority covering the period up to 31 July and employment data from the Annual Population Survey, 2019 (latest data available)

Related question: Why should the government provide income protection in a recession?

How well do these two indicators capture the local economic impact?

As discussed above, the benefit system and the CJRS interact in quite complex ways, which means that the claimant count and CJRS data on their own are unlikely to capture fully the local economic effects. This suggests that we may want to look at both indicators.

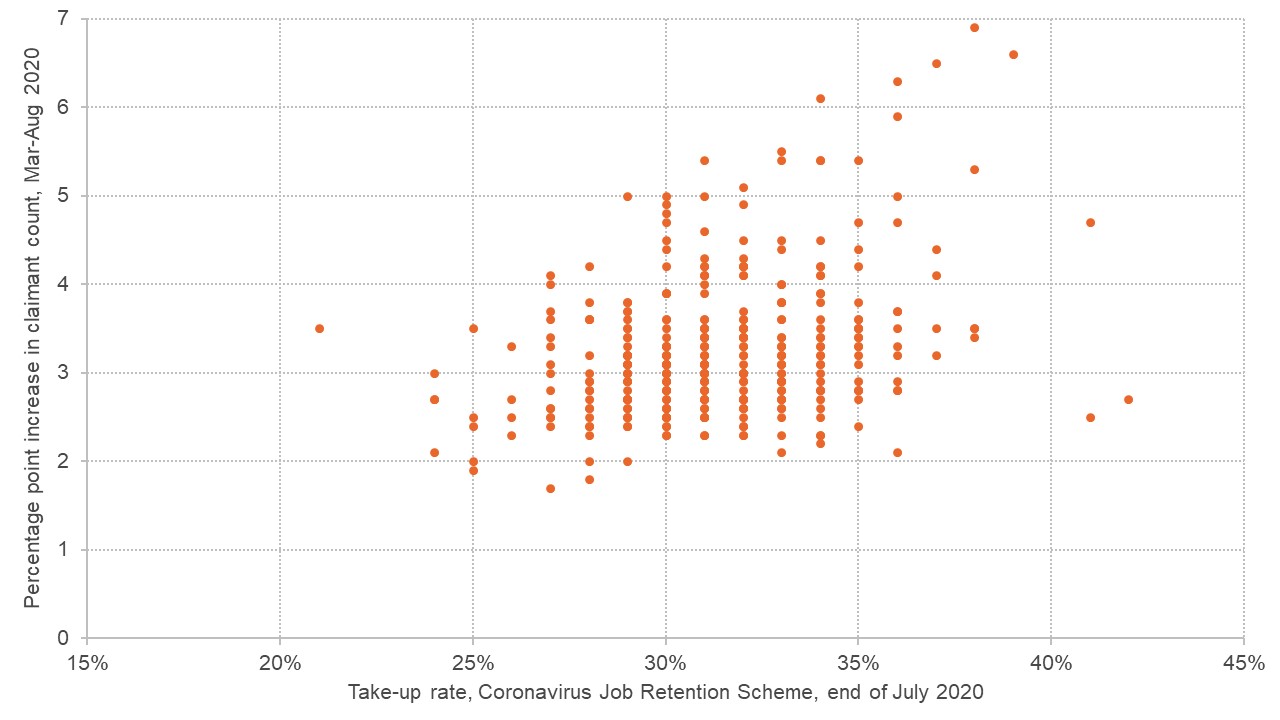

Figure 3 does this by plotting claimant count against CJRS count for all local authorities in Great Britain. One important further caveat applies here. The data that the government released cover the whole period over which the CJRS has been operating, so someone who was initially on furlough but was then made unemployed, would show up in both the claimant and CJRS counts.

Figure 3: The relationship between take-up of the CJRS and the increase in unemployment claims since March 2020 by local authority

Source: Authors’ own calculations based on HM Revenue and Customs statistics on take-up of the CJRS by local authority up to 31 July and Office for National Statistics data on claimant count for March and August 2020, population estimates for 2019 (latest data available) and employment data from the Annual Population Survey, 2019 (latest data available)

Figure 3 shows a positive relationship between take-up of the CJRS and the percentage point increase in unemployment claims since March 2020.

On average, local authorities with a larger take-up of the CJRS also saw the largest increases in unemployment claims since lockdown. This suggests that the CJRS helped to mitigate increases in unemployment in the hardest hit places.

Figure 3 also illustrates a lot of variation around this overall tendency. Understanding what is causing this variation and how it changes over time will be important for getting a fuller picture of the immediate and longer-run local economic effects.

Self-Employment Income Support Scheme

Around 15% of workers in the UK are self-employed. Individuals that have been self-employed for over three years and with earnings below £50,000 are eligible to apply to the Self-Employment Income Support Scheme (SEISS).

Overall, approximately two-thirds of people currently self-employed were eligible. HM Revenue and Customs data show that around 2.4 million self-employed people, approximately 70% of all those eligible, applied for support, which means that a little under 50% of all self-employed people have received support through the scheme.

Does the SEISS data give a good indication of the local economic effects?

HM Revenue and Customs provides local authority data on the percentage of eligible self-employed who are claiming support. There is considerable variation across areas.

Unfortunately, the percentage of the self-employed that are eligible also varies across areas. Data on total numbers of self-employed from the Annual Population Survey are not directly comparable to those used for the SEISS, making it hard to address this problem.

While take-up of the SEISS is an additional source of information about how different local labour markets are being affected, these issues mean that the numbers are a little hard to interpret.

Related question: How is coronavirus affecting the self-employed?

Other sources of data

Despite the caveats above, these three sources of official data are likely to be the most timely and significant indicators of local economic effects. But some other, more experimental sources of data are available. We briefly discuss three here:

Labour market data

Indicators about the current or future state of the labour market, for example, Adzuna’s UK Labour Market Stats provide data on average salaries and vacancies over time for user-specified locations. Similar data are collected by Indeed UK, a popular UK recruitment website.

Adzuna scrapes job adverts from thousands of recruitment sites across the internet, while Indeed monitors its traffic collecting data on job adverts and job searches, clicks and CVs uploaded.

These sources face the usual challenges of other commercial secondary datasets. For example, there may be data quality issues depending on the cross-checking done by the company. The data will reflect the underlying user base and may not be representative.

Movement data

Movement data is often used as a proxy for economic activity. The assumption is that the more people are moving, the more likely they are to be working or spending leisure time and money outside the home.

Some movement data look at how much people are moving based on the location of their phone, for example, data from Google and Apple. Some are based on how they get there, for example, Tomtom’s traffic index and City mapper’s mobility index based on public transport.

Some data are location-based as opposed to user-based – for example, Springboard’s data look at how many people are visiting ‘destinations’ like high streets, shopping centres, etc.

The Centre for Cities high street recovery tracker uses anonymised mobile phone data to measure average footfall in city centres and how this is changing compared with pre-lockdown levels. The tracker is updated monthly and looks at three categories: city centre workers, weekend activity and night-time activity.

These data sources are likely to work well measuring how mobility has been affected by lockdown. Issues will arise when using them as indicators of the local economic effects during the recovery phase and as lockdown measures are gradually lifted.

For example, while some jobs cannot be done remotely (for example, essential workers), others will still be done remotely, affecting the link between movement and local economic activity in a way that is hard to predict. For data sources based on specific types of transport, there will also be issues with modal shift (for example, as people switch from using public transport to cars).

Related question: What has coronavirus taught us about working from home?

Spending data

Spending data are helpful in understanding the impact of the crisis on spending behaviour (see, for example, this article from Tortoise using data from ImFoco). It can be origin-based – which shows how households in different areas have been affected, or it can be destination-based – showing how high streets have been hit and whether strategies to bring people back in and spending are working.

A significant limitation of spending data as an indicator of economic activity is that it may be affected by shifts in shopping behaviour (for example, to online in response to Covid-19).

Related question: What are the key sources of data for measuring the economy in a crisis?

Related question: How can we measure what is happening in the economy now?

Where can I find out more?

Centre for Cities provides a range of Covid-19 resources assessing the effects across cities in England and Wales.

The ONS UK Statistical bulletins provide regional, local authority and Parliamentary constituency breakdowns of changes to UK (un)employment, economic inactivity, and other labour market outcomes. A new release is published monthly, with data lags varying across indicators.

What Works Centre for Local Economic Growth has resources on data for the study of local economies.

Institute for Employment Studies monthly labour market statistics provides analysis of both national and local labour market data

Local differences (responding to the local economic impact of coronavirus): Charlie McCurdy from the Resolution Foundation looks at what might explain the immediate labour market effects across local authorities, with a particular focus on the role of sectoral composition.

What does May’s unemployment claimant count data tell us about how the economic crisis is unfolding? Elena Magrini from Centre for Cities looks at the latest unemployment data and what it tells us about the local economic effects of the crisis.

Who are UK experts on this question?

- Neil Lee, LSE

- Elena Magrini, Centre for Cities

- Henry G. Overman, LSE

- Marianne Sensier, University of Manchester

- Raquel Ortega-Argiles, University of Birmingham

- Phil McCann

- Max Munday

- Helen Simpson

Authors: Elena Magrini, Centre for Cities, and Henry G. Overman, LSE

Update log

30/07/20: Figures updated with latest data from June 2020; minor changes made to some of the text to reflect latest data.

02/10/20: Figures updated with latest data from August 2020; minor changes made to some of the text to reflect latest data.